The most exciting thing happening in commerce isn’t a new marketing channel or payment method. It’s the connection of previously separate systems across the journey from a physical touchpoint to checkout, analytics, and payout status.

For decades, the path from customer interest to collected revenue required stitching together disconnected systems: marketing tools to generate awareness, Action Pages to capture interest, ticketing platforms to process transactions, payment processors to handle money, and payout workflows to deliver eligible proceeds. Each system operated independently, creating data silos, integration complexity, and revenue leakage at every handoff.

The new model is different. Unified platforms now connect the complete loop: physical trigger (QR scan, NFC tap, link click) → digital engagement (landing experience, content, conversion) → commerce transaction (purchase, ticket, signup) → event-payment status (processing, event hold, review, payout). Fewer handoffs mean fewer data gaps.

This isn’t incremental improvement. Connected commerce can provide better attribution, clearer transaction and payout status, and cleaner customer data than fragmented tool stacks.

As GS1 Sunrise 2027 puts QR codes on every product and physical-to-digital engagement becomes universal, the infrastructure that handles the complete loop becomes essential competitive infrastructure.

The Fragmentation Problem

Consider how most organizations handle commerce today:

A customer scans a QR code → The code links to a landing page hosted on one platform → The landing page drives to a ticketing or e-commerce system on another platform → That system processes payment through an integrated payment processor → Funds settle to a merchant account at yet another provider → The business eventually transfers funds to their operating bank account

Each arrow represents a potential failure point:

- Integration between systems requires ongoing maintenance

- Data passes between systems with varying fidelity

- Customer identity fragments across platforms

- Attribution degrades at each handoff

- Settlement delays compound through the chain

- Fees stack at every layer

The operational burden is substantial. Teams manage multiple vendor relationships, maintain multiple integrations, reconcile data across multiple systems, and troubleshoot problems that span multiple platforms. The complexity cost alone is significant.

But the bigger issue is lost value. When systems don’t connect, insights disappear. Which QR placement drove the purchase? What content did the customer engage with before converting? Which scan sources produce highest-value customers? These questions require connected data that fragmented systems can’t provide.

What Complete Loop Infrastructure Looks Like

A unified scan-to-settlement platform handles every stage:

Layer 1: Physical Triggers

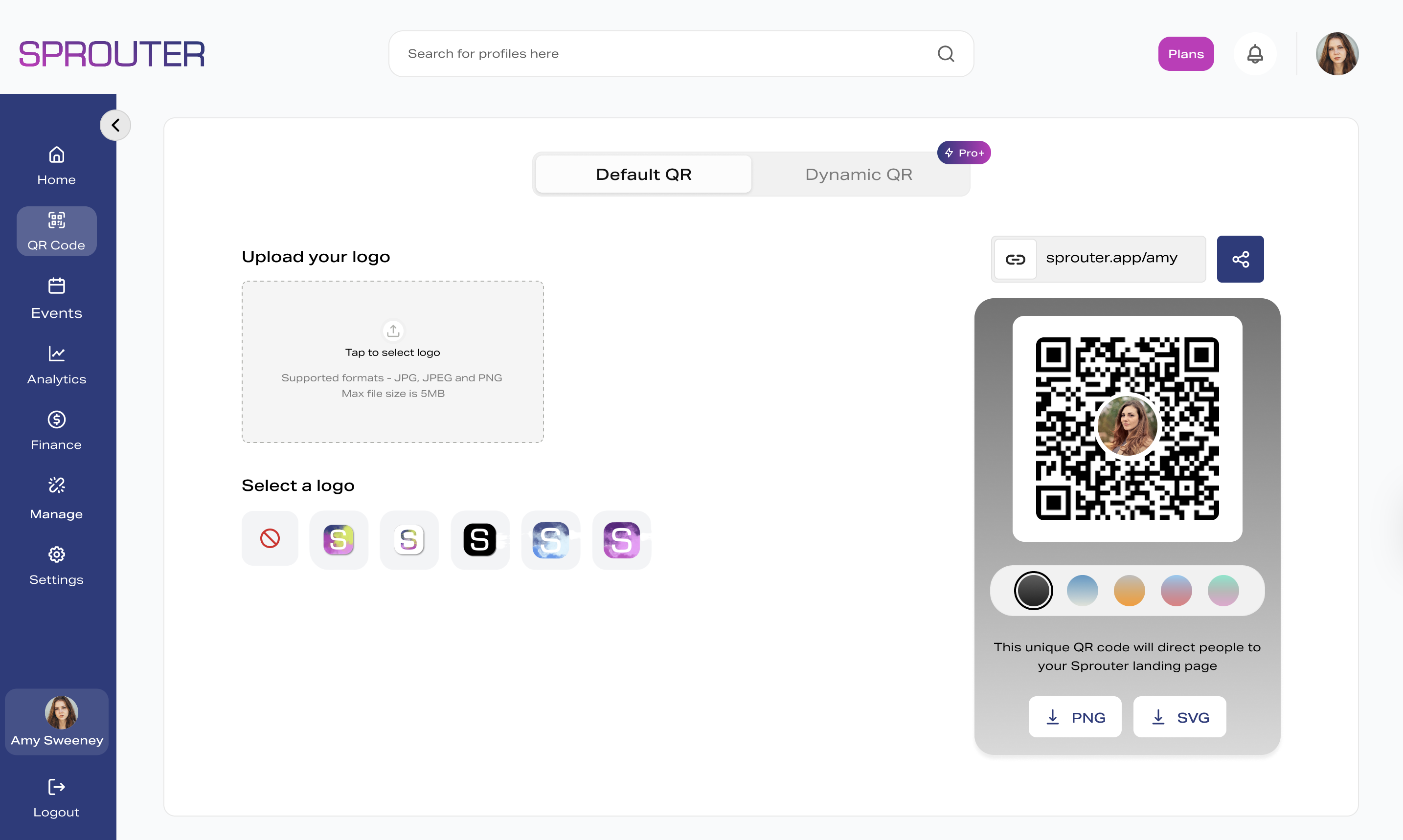

Dynamic QR codes and NFC that serve as measurable entry points. Not just links—intelligent triggers that capture scan context (location, device, time), enable dynamic routing, and connect to unified analytics.

The trigger layer needs to be dynamic (updatable without reprinting) and trackable (every scan captured with context). Static QR codes that simply encode URLs miss both requirements.

Layer 2: Digital Engagement

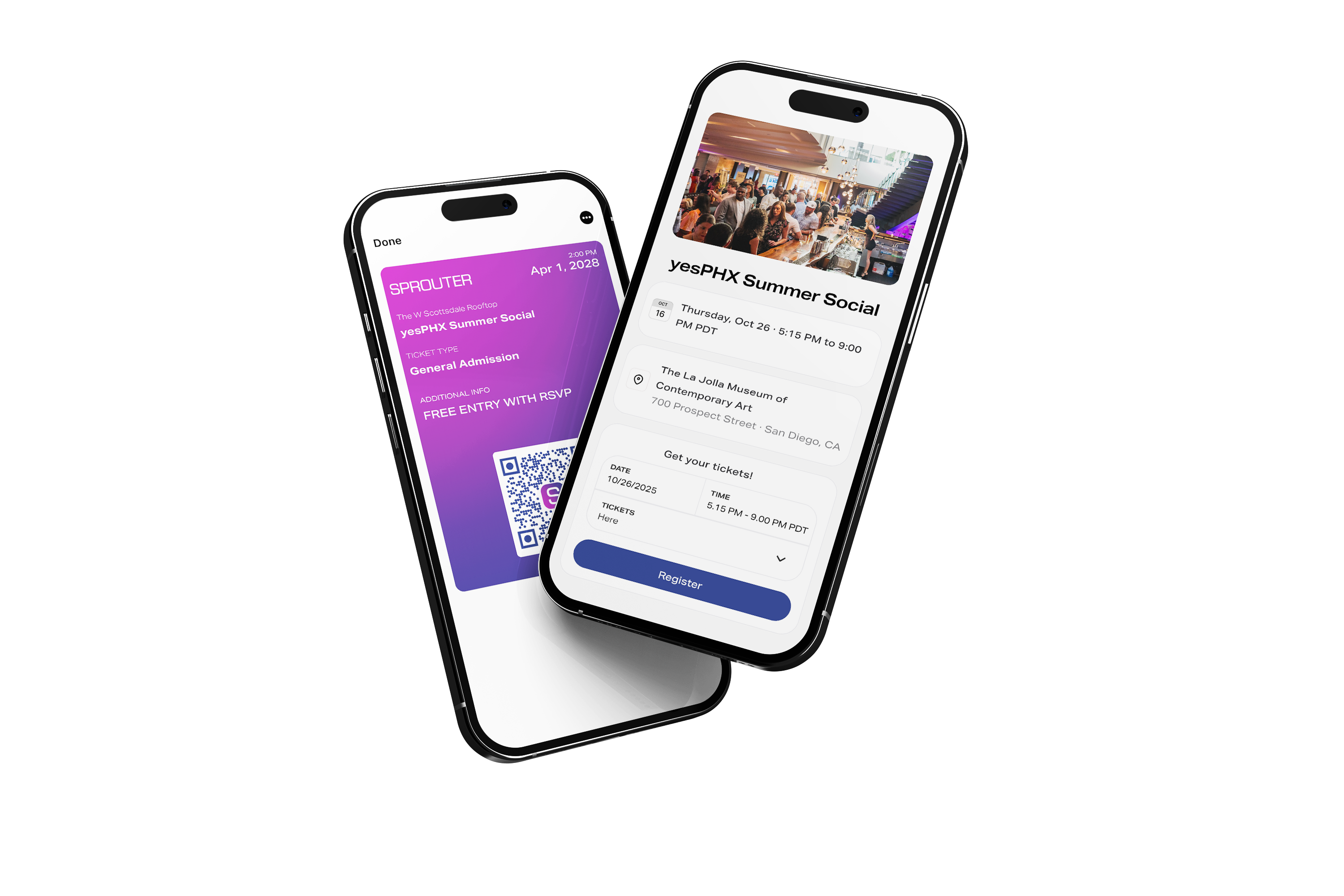

Landing experiences—Action Pages—that engage visitors arriving from physical triggers. Mobile-native, fast-loading, conversion-oriented surfaces that turn scans into actions.

The engagement layer needs flexibility to serve multiple purposes: information delivery, content access, contact capture, social connection, and commerce. Single-purpose landing pages can’t adapt to varied consumer intent.

Layer 3: Commerce and Conversion

Transaction capability native to the platform. Ticket sales, product purchases, registrations, subscriptions—whatever commerce model the business requires.

The commerce layer needs to handle multiple transaction types without external platform integration. Every handoff to external commerce systems introduces friction, fees, and data fragmentation.

Layer 4: Payment Processing

Integrated buyer checkout that connects supported card and digital-wallet payments to the event record and organizer payout status.

For event tickets, the organizer remains the seller and merchant of record while a designated payment processing partner handles supported buyer payments and the applicable event hold.

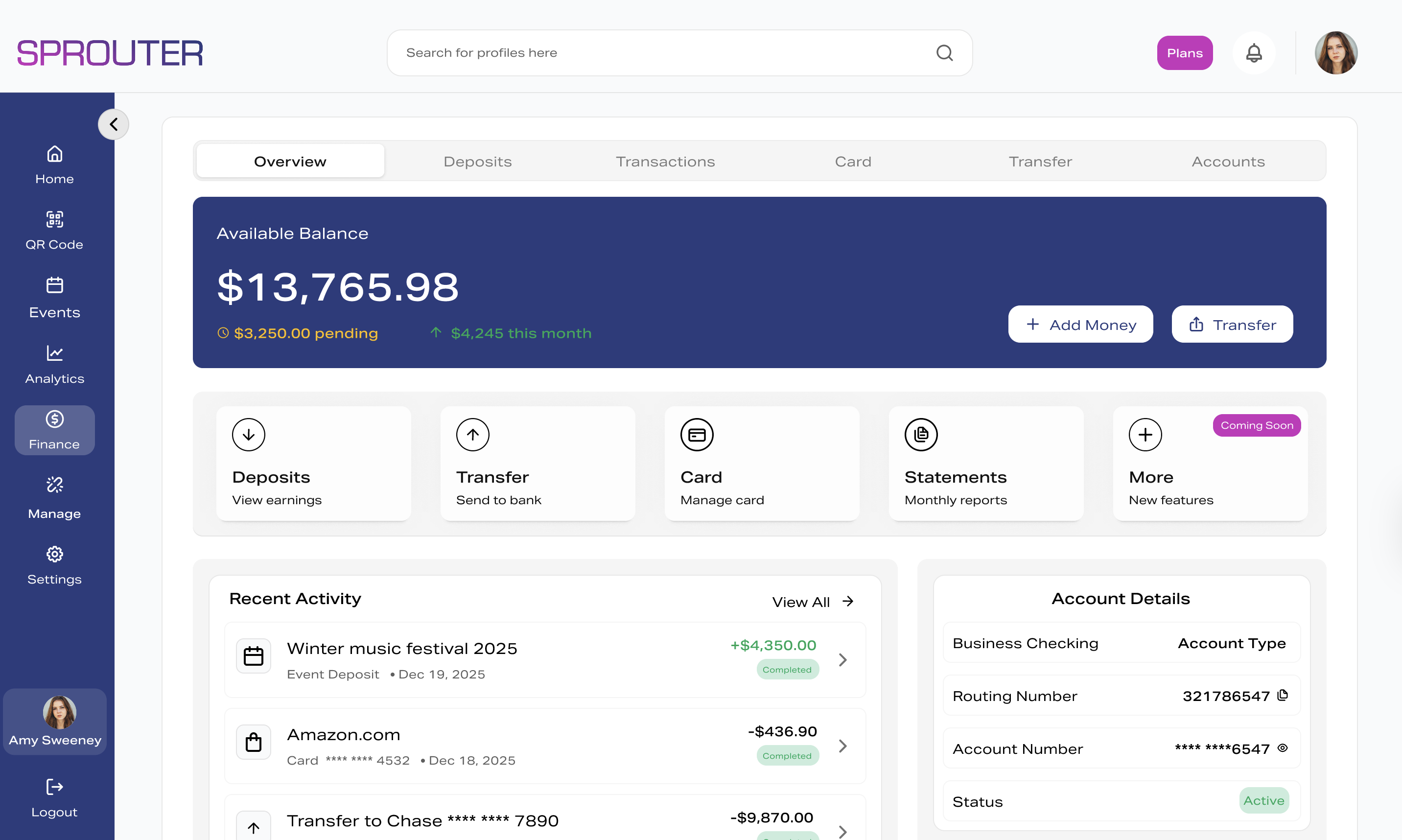

Layer 5: Settlement and Organizer Payouts

A connected workflow that exposes transaction status, the event hold, payout eligibility review, payout initiation, and ACH delivery to an organizer’s linked bank account.

The settlement layer is where important role and timing distinctions appear. Event end, payout eligibility, payout initiation, and ACH delivery are separate steps. Platforms should explain who controls proceeds and when each step occurs.

Layer 6: Analytics Across Everything

Unified measurement connecting every layer. Which triggers drive which conversions? Which engagement content produces which commerce outcomes? Which customer journeys generate which lifetime value?

Analytics need to span the complete loop. Fragmented analytics—separate QR metrics, separate landing page metrics, separate commerce metrics—can’t answer the questions that matter.

The Sprouter Architecture

Sprouter is designed specifically as complete loop infrastructure.

Dynamic QR + NFC: Sprouter’s activation layer handles dynamic QR codes that update without reprinting, NFC tap experiences, and trackable short links. Every scan captures context: device, location, time, scan count, unique versus repeat. Conditional routing sends different scanners to different destinations based on rules you define.

Action Pages: Sprouter’s engagement layer provides Action Pages—mobile-native hub experiences that consolidate links, content, media embeds, contact capture, scheduling, file downloads, and more. They’re built for post-scan context: fast loading, thumb-friendly, action-oriented.

Event Ticketing and Commerce: Sprouter’s commerce layer handles event creation, ticket tiers, capacity management, and transaction processing. Free events build audience. Paid events generate revenue. Both feed the same customer profiles and analytics.

Integrated Payments: Buyers complete supported card or digital-wallet checkout within the Sprouter experience. A payment processing partner processes the transaction and manages proceeds through the applicable event hold and payout review.

Organizer ACH Payouts: The organizer remains the seller and merchant of record. Sprouter acts as the organizer’s limited payment-collection agent under the organizer agreement, but does not have custody or control of proceeds. After the event and payout eligibility review, approved proceeds are initiated by ACH to the linked organizer bank account.

Unified Analytics: Every layer connects through unified analytics. See which QR codes drive ticket sales. Track which Action Page content converts best. Measure which events generate highest-value attendees. Connect the journey from physical scan through transaction and payout status.

The Settlement Workflow

The payout layer deserves special attention because unclear language can blur operational and legal roles.

The current Sprouter event-payment model separates four steps:

Event hold: The payment processing partner has custody and control of ticket proceeds during the applicable hold. Sprouter does not hold the money.

Post-event review: Event end makes proceeds eligible for payout review. Refunds, disputes, reserves, fraud, and risk or compliance review can affect eligibility and timing.

Payout initiation: If proceeds are eligible, an ACH payout is initiated to the organizer’s linked bank account.

ACH delivery: Delivery typically takes 1–3 business days after payout initiation—not after event end—and can be affected by bank holidays and receiving-bank processing.

Sprouter does not provide a stored or spendable organizer balance, deposit account, organizer debit card, or instant payout. The value of the connected workflow is visibility from ticket purchase through payout status—not a banking product.

Attribution That Actually Works

The complete loop enables attribution that fragmented systems can’t provide.

Consider tracking QR code effectiveness. With fragmented systems:

- QR platform tracks scans

- Landing page platform tracks page views

- Ticketing platform tracks purchases

- Payment platform tracks transactions

- Payment partner and bank track payout delivery

Connecting these requires manual data joins, consistent identifier passing, and significant analytical effort. Most organizations approximate rather than actually measuring.

With complete loop infrastructure:

- QR scan creates a tracked session

- Action Page engagement continues the session

- Ticket purchase completes within the same session

- Payment and payout status connects back to the same event record

- Analytics connect the complete journey automatically

You know exactly which QR placement drove which purchase. You can calculate actual ROI by scan source. You can optimize based on real attribution, not estimates.

For GS1 Sunrise, this attribution capability answers critical questions: Which products generate consumer scans? Which scan content drives commerce? Which packaging placements produce best results?

The Competitive Moat

Complete loop infrastructure creates competitive advantages that fragmenting competitors cannot easily replicate.

Speed advantage: Unified systems launch faster than integrated multi-vendor stacks. New campaigns, new events, new products can go live immediately rather than waiting for integration configuration.

Data advantage: Connected systems produce richer data than fragmented alternatives. Better data enables better decisions, better targeting, better optimization.

Cost advantage: Single platform subscriptions typically cost less than multiple vendor fees combined. More importantly, reduced integration maintenance saves ongoing operational resources.

Experience advantage: Customers experience seamless journeys rather than jarring platform transitions. Higher completion rates, better satisfaction, stronger relationship formation.

Settlement visibility: Connected event and payout records reduce manual reconciliation and make it easier to understand where a transaction sits in the workflow.

These advantages compound over time. Organizations operating complete loops improve faster because they learn faster. They optimize more efficiently because they see more clearly. They scale more effectively because they operate more simply.

Who Benefits Most

Complete loop infrastructure provides particular value for:

Event organizers who need promotion, ticketing, check-in, and payout visibility in one system. The traditional stack—separate marketing tools, ticketing platform, payment processor, and payout records—creates unnecessary complexity.

Creators who monetize across content, events, merchandise, and community. Fragmented tools mean fragmented audience data and fragmented revenue streams. Unified infrastructure builds unified fan relationships.

Local businesses with physical locations generating digital engagement. QR codes in-store should connect to loyalty programs, event registrations, and commerce—all in one customer relationship.

Brands approaching GS1 Sunrise who need consumer engagement infrastructure for product QR codes. The codes will exist by requirement; the question is what value they create. Complete loop infrastructure maximizes that value.

Anyone tired of integration hell who wants to stop managing vendor relationships, maintaining API connections, and reconciling data across systems.

The Infrastructure Decision

Every organization faces an infrastructure choice: assemble fragmented tools or deploy unified platforms.

Fragmentation seems flexible—best-of-breed tools for each function, theoretically optimized for specific needs. In practice, fragmentation creates integration burden, data fragmentation, attribution gaps, and operational complexity that erode the theoretical benefits.

Unified platforms seem constraining—one vendor for multiple functions, theoretically less specialized. In practice, purpose-built unified platforms outperform assembled stacks because they’re designed for the connected journey rather than individual functions.

The scan-to-settlement journey is especially integration-intensive. Physical triggers, digital engagement, commerce, payments, and organizer payouts touch many systems a business operates. Fragmentation here is particularly costly.

As GS1 Sunrise 2027 makes physical-to-digital engagement universal, the infrastructure handling that engagement becomes core business capability. The choice of fragmented versus unified shapes competitive position for years to come.

The Complete Loop Imperative

The convergence of physical and digital commerce is accelerating. QR codes on every product. NFC in every smartphone. Consumer expectations for seamless journeys. Business requirements for clean attribution.

Meeting this moment requires infrastructure that doesn’t exist in most organizations today. Assembling it from fragmented tools takes longer, costs more, and performs worse than deploying unified alternatives.

The complete loop—scan to engagement to commerce to settlement—is the new baseline. Organizations that achieve it will operate more efficiently, understand customers more deeply, and capture value more completely than those still stitching together disconnected systems.

The infrastructure decision you make now determines which category you occupy.

Ready for a more connected event workflow? Sprouter brings Dynamic QR Codes, Action Pages, event ticketing, integrated checkout, analytics, and organizer ACH payout information into one platform.